_edited.png)

The SME Trap: Why India's Most Explosive Bull RunWas Never Meant for You

- Shlok Akolia

- 1 day ago

- 19 min read

SME investing in India is not a retail sport. It is a specialised business process. Here is why - and what to do if you still want to play

If you were on Indian Twitter, WhatsApp, or any office WhatsApp group between 2021 and 2024, you saw it.

"SME mein paisa double ho gaya yaar."

"345 times subscribe hua hai, dekhna 100% listing gain."

"Mere CA ne SME IPO ka allotment dilaya, 3 mahine mein 4x."

It was the loudest, most visible, most retail-friendly bull market in Indian history. And it was a trap

Not because SMEs are bad businesses. Some are the next generation of Indian wealth creators. The trap is something simpler, and almost nobody explains it - SME stocks are not built for the retail participant. They are built as a specialised business process for institutions, theme-trackers and professionals with the tools, the timing and the patience to play a structurally illiquid game.

This blog is the long-form explanation of why that is - the boom, the mechanics, the liquidity trap, the governance frauds, the landmines, the goldmines, and the cycles that move like small caps on steroids. By the end, you will know exactly why most retail SME stories end the same way - and what it actually takes to play it.

Part 1: The 2021-2024 SME Boom

Let's start with the numbers. Because the headlines from this period were genuinely insane.

• 247 SME IPOs hit the market in calendar year 2024 alone - more than the previous 5 years combined.

• Over Rs 9,000 crore raised via SME IPOs in FY24.

• Combined market cap on BSE SME + NSE Emerge crossed Rs 3 lakh crore at peak (~Rs 1.84 lakh cr BSE + ~Rs 1.45 lakh cr NSE).

• Subscription multiples that would embarrass mainboard issues - Trafiksol ITS was oversubscribed 345 times. Oriana Power: 176 times. Retail-category subscription on Oriana: 204 times.

How Retail Got Pulled In

The set-up was almost too perfect. Three things came together at the same time:

1.Post-COVID retail mania. Demat accounts in India went from ~4 crore to ~15+ crore between 2020 and 2024. A whole new generation of investors had screens, phones, and a hunger for compounding stories.

2.Listing-day gains became a meme. When stock after stock listed at 80-100% premium - Oriana at +88%, KP Green at +39%, dozens of others doubling on Day 1 - the message to retail was simple: apply karo, paisa free hai.

3.Tip economy went professional. WhatsApp groups, Telegram channels, Instagram reels,

kitty-party SME tip-sharing - an entire ecosystem of "experts" emerged, almost all of them paid by promoters to pump the stock.

By 2024, an SME IPO with a 50x subscription was not news. It was Tuesday. The retail participant believed they had finally cracked the code. The institutions had quietly already started exiting.

Part 2: Why SME Stocks Move Like Rockets (And Crash Like Meteors)

The answer is a single word - float. The shares actually available to trade on any given day. An SME stock often has only Rs 5-15 crore of true tradeable float. That means:

• A single buyer with Rs 2-3 crore can move the stock 20-30% in a session. On a mainboard stock, that same amount disappears into the order book without a trace.

• A coordinated group of 5-6 "operators" can create the illusion of demand, push the price to circuit, and retail FOMO does the rest.

• The same mechanics work in reverse. When one large holder decides to exit, the price falls through every support level because there is no organic buyer at any price.

This is why SME stocks are often called "small caps on steroids". A 1% supply-demand imbalance moves the price 10%. A 2% imbalance moves it 30%. There is no middle gear.

For institutions and professional operators, this is a feature. They can engineer the move. For retail, it is a bug - because by the time the move shows up on the chart, the move is already over.

Part 3: Issue #1 - The Liquidity Trap

This is the single most important fact about SME investing in India. And almost nobody quotes it correctly.

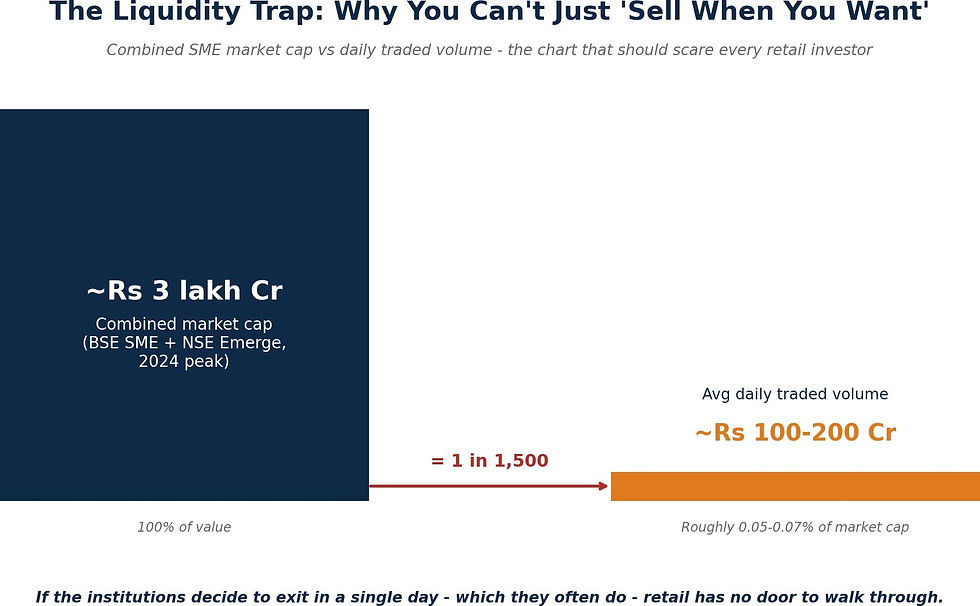

At peak (mid-2024), the combined market cap of BSE SME + NSE Emerge was approximately Rs 3 lakh crore. The average daily traded value across both exchanges was approximately Rs 100-200 crore - on a strong day.

Do the maths. Daily turnover is roughly 0.05% to 0.07% of market cap. Roughly 1 part in 1,500.

For comparison, on the NSE mainboard cash market, daily turnover is roughly 0.5-0.8% of total market cap - 10x the liquidity ratio of SMEs. On large caps like HDFC Bank or Reliance, the ratio is even higher.

Why This Matters for Retail (and Not for Institutions)

Institutions have three exits retail does not:

1. Block deals. Large holders can negotiate off-market trades directly with other institutions, sometimes at a discount, sometimes at a premium. Retail can only sell via the order book.

2. Pre-arranged buyers. Anchor investors and HNI groups often have agreements with promoters and merchant bankers to take exits in tranches over weeks. Retail has no such network.

3. Time. An institution that owns 5% of a stock can take 6 months to exit and is fine with that. A retail investor with Rs 2 lakh in an SME wants the door to open today when the bad news hits. The door isn't there.

When the cycle turned in late 2024 - SEBI tightening, frauds surfacing, momentum reversing - this is exactly what happened. Institutions had quietly exited 6-12 months earlier through block deals and OFS structures. Retail was left holding the bag, watching their portfolio go down 5-10% a day, hitting

lower-circuit after lower-circuit, with literally no buyer on the screen.

Bottom line: the price you see on the screen is meaningless if you can't sell at it. And in SMEs, when you most want to sell, you almost certainly cannot.

Part 4: Issue #2 - The Governance Trap

The second structural issue is older and more obvious - SME-listed companies are held to lower governance standards than mainboard companies. Less disclosure. Less analyst scrutiny. Lower minimum public shareholding. Looser related-party transaction reporting. Smaller audit firms. Less media coverage.

This is by design - it is what makes SME listing accessible to growing businesses. The problem is when it gets abused. And in 2022-2024, it got abused systematically.

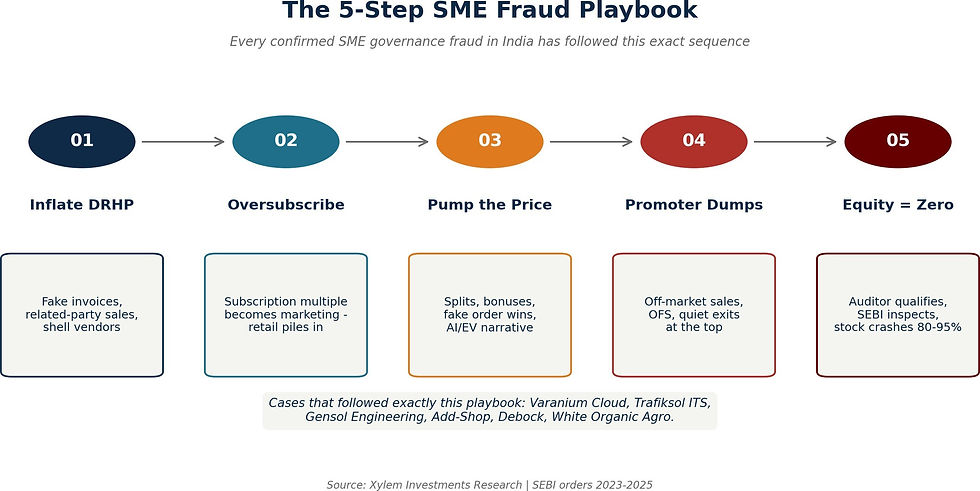

The Playbook That Repeats

Almost every SME governance fraud follows the same five-step playbook. Once you see it, you will not unsee it.

1.Inflated financials in the DRHP. Show eye-popping revenue and profit growth, often through fake invoices, related-party sales, or shell-entity vendor arrangements.

2.Get oversubscribed at IPO. The 100x+ subscription becomes a marketing claim in itself - retail piles in on listing day.

3. Pump the price with announcements. Stock splits, bonus issues, mega-order wins from undisclosed customers, AI / EV / renewables narrative attachments.

4.Promoter dumps shares quietly. Often via off-market transactions or OFS, while public-facing communication remains bullish.

5. Fundamentals revealed; equity goes to zero. Auditors resign or qualify accounts. SEBI inspects. The stock falls 80-95% in weeks. By the time the SEBI order is public, retail is already gone.

Three documented cases will make this brutally clear. We will cover them in detail later in the Landmines section. For now, just note the names - Varanium Cloud, Trafiksol ITS Technologies, and Gensol Engineering.

And these are just the ones SEBI has acted on. The ones that haven't been caught yet are still trading.

Part 5: The 5 SME Landmines Nobody Warns Retail About

Beyond liquidity and governance, there are five structural features of SME investing that quietly destroy retail outcomes. These are not bugs in the system - they are deliberate features designed to filter the segment. They just happen to filter retail the wrong way.

Landmine 1: The Minimum Ticket Size

The minimum SME IPO application size was Rs 1 lakh until March 2025. Then SEBI raised it to Rs 2 lakh. Individual investors must apply for a minimum of 2 lots.

Think about what this means for the typical Indian retail investor. The average retail equity portfolio in India is roughly Rs 4-5 lakh. A single SME ticket is therefore 40-50% of an average retail portfolio - in one illiquid stock. Position sizing is not a choice. It is forced concentration.

Mainboard IPOs let you apply with Rs 15,000. You can build a diversified IPO basket. In SMEs, you are betting nearly half your equity portfolio on a single illiquid micro-cap with limited disclosure. The structure itself is hostile to risk management.

Landmine 2: No Intraday Trading

SME stocks do not support intraday trading. Every buy must be a delivery trade. T+2 settlement only. You cannot exit the same day. You cannot use intraday leverage. You cannot stop out a loser before settlement.

This sounds like a small thing. It is not. It means that if you buy an SME stock at 10am on Monday and bad news breaks at 11am, you cannot sell until at least Tuesday - and very likely the stock will be in lower-circuit by then. The structural exit window is closed.

Landmine 3: Tight Price Bands That Freeze the Exit

Most SME stocks have 5% or 10% daily price bands (upper and lower circuit). On a normal day, this is irrelevant - the stock barely moves. On a panic day, it is everything.

When a fraud surfaces, the stock hits lower circuit at the open and stays there. No sellers because there are no buyers. No buyers because everyone wants to sell. The next day - same thing. The retail investor watches their portfolio lose 5% a day for 10-15 consecutive days with literally no way to exit. By the time the stock finally opens, it is already down 60-80%.

Landmine 4: The Migration Limbo

An SME-listed company must remain on the SME exchange for a minimum of 3 years before it can migrate to the mainboard. Even after that, migration depends on meeting paid-up capital, market cap, profitability and shareholding requirements.

This means that even if a company is genuinely high quality, your investment is structurally locked in the low-liquidity, low-coverage SME exchange for years before any re-rating event. And if the migration doesn't happen on schedule, the stock stays in retail-investor purgatory indefinitely.

Landmine 5: Zero Research Coverage

This is the most underrated landmine. Mainstream brokerages - Kotak, ICICI, Motilal, JM, HDFC Securities

- do not publish equity research on SME-listed companies. Most SMEs have zero analyst coverage. Zero earnings estimates. Zero published target prices.

What does that mean for you, the retail investor? It means the only source of information on the company is - the company itself. There is no independent professional checking the numbers. No external auditor of the auditor. No analyst asking uncomfortable questions on the concall. It is you versus the promoter. Guess who wins that game.

Part 6: The SME Goldmines – When It Actually Worked

Now to be fair – SME investing absolutely produced goldmines in the 2021-2024 cycle. Some of the best small-cap wealth creators in modern Indian markets came directly from this ecosystem, either as SME listings or as ecosystem beneficiaries of the SME boom.

Three stories make the point – and each one has the chart to prove it.

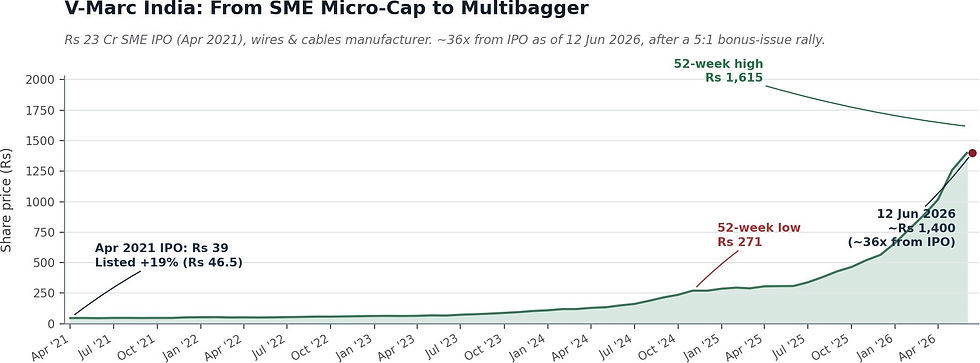

Goldmine 1: V-Marc India – From Rs 23 Crore SME IPO to a 36x Multibagger

V-Marc India listed on the BSE SME platform in April 2021 with a tiny Rs 23 crore IPO – a

wires-and-cables manufacturer nobody outside the segment had heard of. The IPO priced at Rs 39 and listed at Rs 46.5, a modest +19% day-one pop, nothing like the triple-digit listing gains that grabbed headlines elsewhere in the SME space.

The real story took years to play out. From under Rs 50 through 2021-2023, the stock began compounding as the company’s order book and margins improved, then accelerated sharply through 2025 on a renewedcapex/infrastructure-spending narrative and a 5:1 bonus issue that pulled in fresh retail attention. It hit a 52-weekhigh of ~Rs 1,615 in June 2026 before settlingaround ~Rs 1,400 – still roughly 36x the IPO price five years on. The lesson here is patience, not entry timing: V-Marc rewarded the few investors who held a genuinely illiquid SME micro-cap through multiple flat years, not the ones chasing the listing-day pop.

Goldmine 2: Oriana Power – The Retail Frenzy That Actually Worked

Oriana Power’s SME IPO in August 2023 was a masterclass in why SME investing seduces retail. The issue was oversubscribed 176.58 times overall – retail category subscribed 204 times, NII 251 times, QIB 72 times. The grey market premium was ~88% on listing day.

The post-listing story has been genuinely strong – solar EPC tailwinds, expanding order book, real revenue growth. The stock kept compounding well past listing day, eventually peaking at ~Rs 3,064 in November 2025 – roughly 26x the IPO price, a little over two years after listing. It has since corrected hard to a 52-week low of ~Rs 1,500 in March 2026, and now trades around ~Rs 1,585 (~13.4x from IPO as of 11 June 2026). Oriana is one of the few SME boom-era names that has held up structurally even after a sharp drawdown from its highs. It is also the exception, not the rule. For every Oriana, there are 5-10 SME IPOs from the same window now trading 60-80% below their highs.

Goldmine 3: KP Green Engineering – The Group With a Proven Playbook

KP Green Engineering’s BSE SME IPO in March 2024 raised Rs 189.5 crore – 29.5 times oversubscribed – and listed at Rs 200 against a Rs 144 issue price (+39% on debut). The stock kept climbing through 2024 and 2025, peaking at ~Rs 626.65 in November 2025 (~4.3x from IPO), before correcting to a

52-week low of ~Rs 301 in March 2026. It now trades around ~Rs 393 (as of 19 June 2026) – still roughly 2.7x the IPO price.

But the more interesting story is the KP Group’s track record. Both their prior SME listings – KP Energy (2016) and KPI Global Infrastructure (2019) – have already migrated to the mainboard and rewarded long-term holders multi-fold. The group has built a playbook – raise on SME, prove the business, migrate, re-rate. That repeatability is rare. And it is why disciplined SME investors track promoter pedigree before they track price.

Part 7: The SME Landmines-When the Trap Sprang

Now the other side. The same exchange, the same boom, the same retail enthusiasm produced multiple complete equity wipeouts in 18 months. Three stories make the case.

Landmine 1: Gensol Engineering - 22x to 95% Down

Gensol is the cleanest, freshest case study of how an SME-era retail favourite can implode. Note - Gensol is technically mainboard-listed, but the entire retail story around it - the EV pivot, the renewable narrative, the BluSmart association - was classic SME-era retail psychology in motion.

The bull run was real. From ~Rs 50 in early 2021 to a peak of ~Rs 1,124 in September 2024 - roughly a 22x bagger in 3.5 years. Retail piled in on the EV charging + green hydrogen + BluSmart partnership narrative. Then SEBI's April 2025 order landed.

The findings were jaw-dropping:

• Promoters Anmol Singh Jaggi and Puneet Singh Jaggi accused of siphoning approximately Rs 262 crore out of Rs 978 crore in loans from IREDA and PFC - money meant for purchasing 6,400 EVs for BluSmart.

• Only 4,704 EVs were actually purchased against the loan covenant. The ~Rs 207 crore gap was rerouted through related-party entities.

• Rs 43 crore went to DLF Ltd toward purchase of a luxury apartment at The Camellias in Gurgaon.

• Personal expenses included Rs 26 lakh on a golf set, Rs 17 lakh on shopping at Titan, and Rs 10+ lakh on spa sessions.

The stock crashed from Rs 1,124 to roughly Rs 51 by December 2025 - a ~95% wipeout. Both Jaggi brothers were barred from capital markets and resigned. Retail holders who averaged down at Rs 600, Rs 300, Rs 150 on the same comforting "acchi company hai, bounce back karega" narrative - watched their entire position go to near-zero.

Landmine 2: Varanium Cloud - Selling Data Centres That Did Not Exist

Varanium Cloud is the SME fraud story that should be taught in business school. Listed on BSE SME in September 2022 with a ~Rs 40 crore IPO. Claimed business: data centres, distance learning, payment gateways, IT-infrastructure-as-a-service. Sound modern. Sound scalable. Sound legitimate.

The stock pumped roughly 9x in 9 months - from ~Rs 70 to ~Rs 650 - on stock splits, grand expansion announcements, and bullish forwards across retail channels.

Then NSE's inspection team actually visited the company's claimed data centre locations. They found nothing. Empty premises. Near-zero electricity consumption (data centres are extremely

power-intensive). At another site - no data centre at all. SEBI's findings:

• Promoter Mr. Sabale syphoned off the entire IPO proceeds to other entities.

• Financials were fabricated to show business activity that did not exist.

• Stock-split announcements + share-price pumping let the promoter dump shares at the top - net gain Rs 122.76 crore.

• Over 10,000 retail investors lost money. SEBI's confirmatory order (October 2024) barred Varanium Cloud and Mr. Sabale from markets permanently.

The stock is now around Rs 30 - down ~95% from peak. The retail investors who bought on "Sir bola hai pakka multibagger hai" have no recovery. Equity-fraud cases in India settle, on average, with retail receiving cents on the rupee, years after the event.

Landmine 3: Trafiksol ITS - SEBI's First Ever IPO Cancellation

This one is historic. Trafiksol ITS Technologies opened its BSE SME IPO in September 2024, offering intelligent transportation systems for traffic and toll management. Subscription multiple: 345.7 times. Money raised: Rs 44.9 crore. Listing was scheduled.

Before the stock could be listed, SEBI received a complaint from the Small Investors' Welfare Association (SIREN). Investigation revealed that a key third-party vendor mentioned in the prospectus was a shell entity with a fabricated profile and forged financial statements.

SEBI's response was unprecedented - they cancelled the IPO before listing. Ordered Trafiksol to refund the entire Rs 44.9 crore to investors within a week, with interest. This was the first time SEBI has cancelled an IPO and ordered a refund post-subscription.

The Trafiksol case is important for one specific reason - it shows that even 345x oversubscription is not a quality signal. The herd will rush into a stock based on listing-gain expectation, with zero scrutiny of the actual business or the disclosed counterparties. SEBI's intervention was the only thing that stood between retail and yet another total loss.

And honestly - the same pattern (shell vendors, fabricated counterparties, related-party round-tripping) almost certainly exists in many other SME issues that haven't been investigated yet. Trafiksol is the case that was caught. The cases that haven't been caught are still trading and still being averaged down by retail.

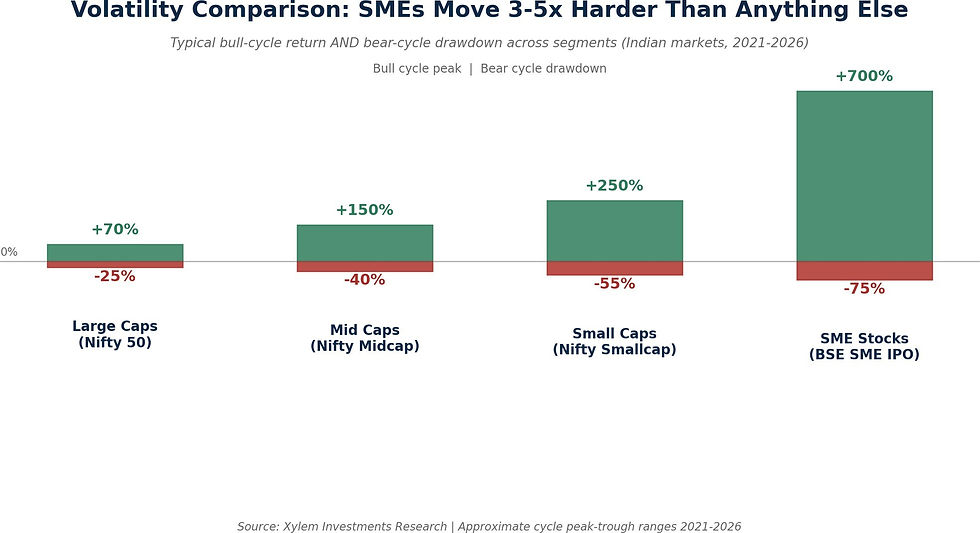

Part 8: SME Cycles = Small-Cap Cycles on Steroids

If small-cap stocks move 2-3x faster than large caps in a bull market, SME stocks move 5-8x faster. The same momentum that takes a Nifty stock up 30% in a year takes a typical SME multibagger up 300% in 9 months. The same correction that drags small caps down 25% drags SMEs down 60-80%.

This is not market commentary. It is the structural consequence of everything we have discussed so far - tiny float, no research coverage, zero institutional cushion, and the price-band mechanics that make exits binary.

When you map out the actual SME cycles in India, you see four distinct phases in the last decade - each one bigger and faster than the last.

Cycle 1: 2016-2018 - The First Taste

The first real SME bull run. Demonetisation (November 2016) created a huge formalisation tailwind for small businesses. The first wave of tip-driven retail entered SME IPOs. The cycle ended with the IL&FS default in September 2018 - which choked NBFC funding, killed sentiment in micro-caps, and put SMEs into a deep freeze.

Cycle 2: 2018-2020 - The Long Bear

For two years, SMEs went through what professionals call a time correction PLUS a price correction. The double whammy.

Time correction: Stocks went sideways for 18-24 months. Even fundamentally decent names refused to move. Capital was technically intact but compounding quality was destroyed - because zero return for 2 years is itself a massive opportunity cost.

Price correction: The lower-quality names saw 50-80% drawdowns from their 2018 highs. Many never recovered. COVID in March 2020 was the final clean-out.

Retail who held through this period and didn't add at the bottom underperformed even fixed deposits.

Cycle 3: 2021-2024 - The Mega Cycle

The big one. Post-COVID monetary stimulus + retail demat explosion + government renewables/EV/defence push + SME tax benefits + general financialisation - everything aligned at once. The BSE SME IPO Index roughly 10x'd between mid-2021 and early 2024.

This was the cycle where genuine wealth was created. KP Group, Oriana Power, multiple solar / EMS / EV-adjacent names, and the broader Waaree ecosystem all delivered generational returns. It was also the cycle that pulled in the largest, most unprepared cohort of retail investors in Indian SME history.

Cycle 4: 2024-2026 - The Reality Check

The current bear. The trigger sequence was textbook: SEBI tightened SME IPO norms in late 2024, frauds (Varanium, Trafiksol, Gensol) started getting exposed, momentum reversed, institutional money exited via block deals, and retail was left holding the bag. The BSE SME IPO Index is currently down

~40-50% from 2024 peak, with the lower-quality names down 70-90%.

The most important lesson from this cycle structure: in SMEs, when you enter matters more than what you buy. A great business bought in the wrong part of the cycle loses 60% on the way to becoming valuable. A mediocre business bought at cycle bottom triples on momentum alone. Entry timing is the single largest determinant of SME outcomes.

Part 9: How to Actually Win in SMEs (If You Must)

So if SMEs are a trap for retail, what does the small minority of professional SME investors who actually make money do differently? Three things.

Method 1: Catch the Theme Before the Crowd

Every SME mega-bull run is anchored on one or two structural themes that the broader market is just starting to notice.

• 2016-2018 - first formalisation wave + GST beneficiaries

• 2021-2024 - renewables (solar EPC, BOP, wind), EV ecosystem, EMS / contract manufacturing, defence indigenisation

• The next cycle will be different - possibly advanced materials, semiconductor ecosystem, agritech, climate tech, or precision manufacturing. Nobody knows yet.

Professional SME investors spend months before the cycle turns talking to suppliers, mapping value chains, reading government policy documents, attending unsexy industry conferences. They identify the theme 12-18 months early and accumulate quietly. By the time WhatsApp groups are forwarding tips on the theme, the smart money has already entered.

Method 2: Catch the Cycle, Not the Stock

The corollary of the cycle data above - in SMEs, the cycle decision matters more than the stock decision. A 60% allocation to a basket of average SME names bought at cycle bottom will beat a 100% allocation to the best SME name bought at cycle top.

Professional cycle reading involves multiple signals - new SME listing volumes, retail subscription multiples, grey-market premium dispersion, BSE SME index momentum, broader small-cap valuations, RBI liquidity stance, SEBI's regulatory posture. When most of these flash red simultaneously, the cycle is at top. Early 2024 was that moment. Most retail was just entering.

Method 3: Treat It as a Business Process, Not a Trade

The reason SMEs are a specialised business process and not a retail trade comes down to scale and process requirements:

• Forensic accounting capability - ability to read related-party notes, reconcile cash flow to profit, spot revenue recognition aggression.

• Channel-check infrastructure - physically visiting plants, talking to distributors, calling competitors, verifying customer relationships.

• Promoter due diligence - background checks, prior venture track record, related-party ownership maps.

• Position sizing discipline - no single SME position above 2-3% of portfolio, no thematic concentration above 15-20%.

• Exit triggers - pre-defined fundamental and technical signals that force action regardless of conviction.

Doing this for one stock takes weeks. Doing it for a portfolio of 8-12 SME positions takes a team. This is the work that retail simply cannot replicate alone - not because retail is unintelligent, but because the time and infrastructure requirements are full-time-professional-level.

Part 10: The Bare-Minimum Forensic Checklist for Retail

Suppose you have decided, despite everything in this blog, that you still want to invest in an SME yourself. Fair enough. Here is the minimum due diligence before you click "Buy". Skip even one of these- skip the stock.

Quick Explanation of Each Check

1. Promoter pledge %. Check BSE / NSE filings under shareholding pattern. Anything above 25% pledged is a hard pass. Promoters pledge when they can't raise capital cleanly - that is information.

2. Auditor independence. Check the auditor name in the annual report. If it is a Big-4 or top-tier regional firm, fine. If it is a small, unknown firm and the auditor has changed recently - walk away.

3. Modified audit opinion. Read the auditor's report. "Qualified opinion" or "emphasis of matter" sections are the auditor formally telling you they have concerns. Take them seriously. Most retail never reads this section. Read it.

4. Related-party transactions. Notes-to-accounts will list transactions with promoter-controlled entities. If more than 15-20% of revenue or expenses runs through related parties - red flag.

5. Cash flow vs profit. Is the company reporting net profit but no operating cash flow? Compare 3 years of P&L net profit with 3 years of cash flow from operations. Persistent divergence = manufactured earnings.

6. IPO fund usage. SEBI now requires quarterly utilisation reports. Compare actual spending to the original DRHP plan. Diversions are a giant signal.

7. Director / KMP exits. Stock exchange filings disclose senior resignations within 24 hours. A CFO or company secretary leaving suddenly is the single most reliable governance red flag in markets.

8. Promoter selling post-lock-in. Check insider trading disclosures. If promoters are selling on the way up, you should be too. They know what you don't.

None of this is theoretical. Every single one of the SME disasters we covered above had at least 4-5 of these red flags visible on official filings before the stock crashed. The information was free, public, and ignored - because retail rarely reads it.

How Xylem Thinks About the SME Opportunity

At Xylem Investments, our position on SMEs is straightforward - the segment is a genuine alpha pool, but only when treated as a specialised business process. We do not run an SME-only product, but we actively track the segment as part of our small and mid-cap thematic work. Specifically:

• Theme-first, then stock. We identify the 2-3 structural themes likely to dominate the next SME cycle before they are obvious - and map the value chain top-down.

• Forensic before fundamental. Every SME candidate goes through a forensic accounting pass, channel checks, and promoter due diligence before we even open the financial model.

• Cycle-aware sizing. Position sizes scale up only when our cycle indicators support it. In late-cycle phases, exposure gets cut even on names we still like fundamentally.

• Liquidity-first exits. Every SME holding has pre-defined exit triggers and a phased exit plan - because you cannot wait for the headline to sell in this segment.

If you'd like to understand how this framework works in practice - or if you have a meaningful SME allocation that needs an objective second look - you can explore our approach on the Xylem website or schedule a portfolio review. We don't make promises about future returns. We do promise an unflinching read of where you stand.

Putting It All Together

1 SMEs are not a retail product. They are a specialised business process – thin float, no coverage, structurally illiquid. The retail playbook does not work here.

2 The 2021-2024 boom was real, and the trap was real. 247 IPOs in 2024 alone, Rs 3 lakh crore combined market cap at peak, 345x oversubscription multiples – the cycle was historic. Most retail entered exactly when the institutions were quietly exiting.

3 Liquidity is the silent killer. Rs 3 lakh cr peak market cap vs ~Rs 100-200 crore daily turnover. Roughly 1 part in 1,500. When you most want to sell, no buyer exists.

4 Governance frauds are systemic, not isolated. Varanium Cloud, Trafiksol ITS, Gensol Engineering, Add-Shop, Debock – five named SEBI cases in 18 months. The pattern is identical. The ones not yet caught are still trading.

5. 5 hidden landmines compound the damage. Rs 2 lakh minimum ticket, no intraday, tight price bands, 3-year migration lock-in, zero research coverage. The structure is hostile to retail by design.

6 Goldmines exist – for the prepared. V-Marc India, Oriana Power, KP Group. Each one rewarded investors who entered early on a theme and had the conviction to hold through volatility.

7 SME cycles are small-cap cycles on steroids. Four distinct cycles in 10 years – 2016-18 bull,

2018-20 bear, 2021-24 mega bull, 2024-26 bear. Entry timing matters more than stock selection.

8 If you must invest, run the 8-point forensic checklist. Promoter pledge, auditor quality, modified opinions, related parties, cash flow vs profit, IPO fund usage, KMP exits, promoter selling. Skip one – skip the stock.

SME investing in India is a game with great prizes for the prepared and total ruin for the unprepared. The deciding factor is not luck. It is process.

If you'd like to discuss your portfolio or explore how Xylem can help you navigate this market, consult with us here.

Comments