_edited.png)

The Oracle of Doomed Bubbles

- Nayan Bhodia

- Nov 17, 2025

- 9 min read

Few investors carry the kind of gravitational pull Michael Burry commands. He is a quiet anomaly, a financial oracle who speaks rarely, trades quietly, disappears often, and yet his footprints shape the loudest, most critical debates in global markets. When Burry takes a position, it isn’t a passive trade; it is a worldview rendered in derivatives. His shorts are not just transactions; they are definitive judgments on the cycle, the incentives, the behaviour, and the collective blindness embedded into the financial system.

Over two decades, Burry has done battle with four of the largest market mispricings of our era:

1. The Dot-Com Collapse (2000-2001): Where he absorbed the foundational lesson of the value investor.

2. The Housing Crisis (2008): His defining triumph over structural incentive failure.

3. The Post-COVID Mania (2021): The integrated attack on pure liquidity addiction.

4. The AI Bull Run (2023-2025): The current short against mega-cap concentration and valuation math.

And contrary to popular legend, Burry did not merely "refuse to participate" in the dot-com mania. He executed the perfect dual strategy: while buying deep value stocks, he also shorted the overvalued hype to secure his first legendary returns. This long, complete history, not the Hollywood or Twitter version, is the actual, structured, economic, behavioural, and financial evolution of Burry’s thinking. It is the story of a genius who profits when systems fail.

TALE 1 - THE DOT-COM LESSON (1999-2001)

Before he shorted the housing market, he mastered the world by deploying a dual strategy during the dot-com bubble.

Most people correctly understand that Burry shorted the dot-com bubble, it was his first major win and the basis for his legendary returns. He didn't just refuse to touch it; he actively bet against it, identifying the spectacular valuation fraud in the technology sector.

In late 2000, as the market euphoria peaked, Burry launched his hedge fund, Scion Capital. His investment thesis had two simultaneous parts:

1. The Short Bet (Defense): He opened short positions against the most egregious, loss-making, high-flying tech stocks whose valuations defied all logic and financial fundamentals. This was his hedge against madness.

2. The Long Bet (Offense): Following a strict, deep-value Ben Graham-style approach, he bought deeply discounted community banks, obscure industrials, and small-cap value names. These "Net-Net" stocks were often trading for less than the net cash on their balance sheets, offering a massive margin of safety.

While speculators were being wiped out by the collapse, Burry's portfolio did not just survive, it soared. He was perfectly positioned: his short positions made massive gains as the NASDAQ crashed 80%, and his long positions were intrinsically cheap, preventing their prices from falling further.

He wasn't mocked for "not getting it"; he was celebrated for his brilliant, contrarian vision, a doctor-turned-investor who beat the Wall Street elite at their own game.

Scion Capital, launched in 2000, returned 55% in 2001, as against the NASDAQ’s big crash:

TALE 2 - THE BIG SHORT (2005-2008)

Michael Burry's most famous trade was not merely a lucky prediction that home prices would fall; it was a deeply researched, high-conviction bet against the moral and structural integrity of the entire modern financial system.

The Problem: A System Built on a Lie

Beginning his investigation in 2005, Burry realized that the American mortgage market was resting upon a single, catastrophic flaw: the universal belief- held by banks, rating agencies, and investors-that U.S. home prices would never decline nationally. This allowed institutions to engage in reckless behavior.

Burry's Unique Research

While Wall Street focused on complex, top-down models, Burry performed the manual, granular work that no one else dared to do:

● Loan Tape Analysis: He secured the raw data for thousands of individual subprime mortgages, meticulously studying the actual payment histories of borrowers.

● The Crucial Discovery:

His analysis showed that borrowers were defaulting (stopping payments) at alarming rates, and critically, this was happening before their low, introductory "teaser rates" reset to much higher payments. This proved the fundamental underwriting quality was non-existent and the mortgages were toxic from day one.

The Architecture of Failure

Burry recognized the process of turning bad mortgages into "safe" bonds was a chain of broken incentives:

1. Origination: Mortgage brokers were paid to generate volume, not quality, leading them to issue loans to anyone, regardless of ability to pay.

2. Securitization: Investment banks bundled these low-quality, high-risk loans into instruments called Mortgage-Backed Securities (MBS) and then repackaged them again into complex CDOs (Collateralized Debt Obligations).

3. Validation: Rating agencies, who were paid by the banks issuing the bonds, assigned AAA ratings (the safest designation) to the majority of these CDO tranches. They ignored the fundamental data, allowing garbage to be stamped as gold.

The Trade: Inventing the Counter-Bet

Convinced the collapse was inevitable, Burry sought to short the system, but the standard instrument didn't exist for this complex debt.

● Custom-Built CDS: He worked with major banks to purchase bespoke Credit Default Swaps (CDS), an insurance policy against the failure of the specific, highly vulnerable mortgage bonds he identified. He was, in effect, inventing the very instrument needed for the trade.

● The Isolation: For nearly two years, Burry paid millions in premiums, watching the market soar while he was ridiculed. This led to a near-mutiny by his investors, who demanded their capital back. Burry had to stand completely alone against the entire financial world based on the strength of his data.

The Payoff

When the housing market finally cracked in 2007, the "safe" AAA-rated tranches of the mortgage bonds began to fail. The US markets fell by ~55% when the bubble burst. Burry's patience and precise positioning paid off spectacularly: his CDS contracts rapidly multiplied in value, ultimately generating over $700 million in profits for his fund. His success was the result of a profound ability to disregard consensus and place his faith solely in unbiased, primary research.

TALE 3 - THE POST-COVID MANIA (2019-2022)

The three years following the 2020 crash were not defined by recovery; they were defined by a giddy, reckless fever dream. The authorities flooded the system with so much free money, trillions in Quantitative Easing, stimulus checks, and the promise of zero interest rates forever-that they effectively canceled the law of financial gravity.

Risk vanished. Work felt optional. The stock market stopped feeling like an investment tool and transformed into the world's most accessible casino.

The new reality was intoxicating:

● The Addiction: Every dip was instantly bought. Every day felt like a guarantee of profit. This predictability fostered a terrifying addiction to liquidity.

● The Culture: Reddit pages became trading floors. Young, first-time investors used zero-fee apps like Robinhood to buy call options-massive, highly-leveraged bets that they would often win overnight. Crypto coins with dog mascots minted millionaire paper fortunes.

● The Delusion: Companies with no revenue and no prospect of profits were trading at multi-billion dollar valuations because "The Story"-the narrative of disruption-was all that mattered.

This wasn't just a bubble; it was a full-blown psychological mania.

Michael Burry, the doctor who sees pathology in finance, stood outside this crowded, boisterous casino. He didn't see innovation; he saw the same four, dangerous symptoms he'd witnessed in 2007:

1. Addicted investors,

2. Blind cheerleaders,

3. Risk-free leverage,

4. Fatal hubris that prices only go one way.

While the world was celebrating, Burry was coldly putting on his full protective gear. His mission this time was to short not just a handful of faulty bonds, but the entire, infected architecture of market belief itself. He was betting on the one force that always returns: gravity.

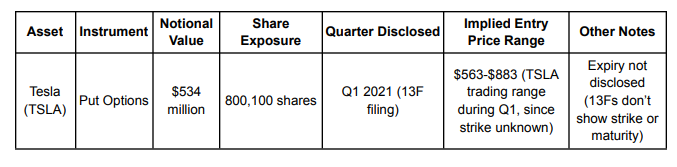

One of his shorts was:

1. TESLA

Thesis

Valuation disconnected from fundamentals: Tesla traded at a 646B market cap with negative EBIT, while 32 automakers with 102B EBIT were valued only slightly higher.

Revenue mismatch: Tesla’s 24.5B revenue was tiny compared to the industry’s 2.3 trillion, yet the stock price assumed long-term leadership far ahead of reality.

Speculation premium: A PE ratio above 600 showed the stock was driven by hype and momentum rather than underlying cash flows.

Future priced in too early: Even with 40 to 50 percent annual growth, fundamentals would take nearly a decade to match the valuation.

Short-term bubble setup: Burry expected the stock to cool off before fundamentals improved, making this a valuation timing short, not a bet against Tesla’s business.

A few Others

Analytical Category |

ARK Innovation ETF (ARKK) |

iShares 20-Year Treasury ETF |

I. Core Thesis & Valuation Flaw |

|

|

Primary Target | Speculative Valuation: Targeting the price of long-duration growth stocks that rely on future potential. | Monetary Policy/Inflation: Targeting the price of long-term debt that relies on low interest rates. |

Fundamental Flaw | Valuation Disconnect: ARKK's top holdings traded at astronomical multiples (e.g., P/FCF ratios of 100-300), pricing in an unrealistic future growth that lacked current free cash flow. | Mispricing of Risk: TLT was mispriced for rising inflation and required Federal Reserve tightening, offering an asymmetric downside (more room to fall than rise). |

II. The Mechanism (Duration Risk) |

|

|

Definition of Risk | Equity Duration Risk: Growth stocks are sensitive to interest rates because the bulk of their estimated value lies in distant cash flows. | Bond Duration Risk: Long-dated bonds (20+ years) have the highest duration, making them extremely sensitive to even small rises in interest rates. |

Betting Mechanism | Profits from the collapse of growth valuations when the discount rate rises. | Profits from the fall in bond prices caused by the necessary interest rate hike. |

III. Strategic Conviction & Data |

|

|

Total Exposure | $31 million Notional Value against 235,500 ARKK shares. | Notional value not disclosed, but he increased his put position by 53 percent in Q2 2021. |

Conviction Metric | The short was a judgment against the entire narrative-driven investing philosophy embodied by the fund's manager and investor base. | The 53% increase in puts demonstrated a high-conviction bet against the Fed's "transitory inflation" consensus, betting on a forced policy pivot. |

The oracle strikes again:

If the housing trade was Burry’s “big short”, the AI trade is his “loudest warning”.

In his latest 13F filing, Scion Asset Management has effectively turned into a concentrated macro bet against the AI leaders.

As of the September 2025 quarter, Scion disclosed:

Stock | Instrument | Notional value* | Underlying exposure | Approx premium paid | Expiry profile |

Palantir | Puts | 912 million USD | 5 million shares | About 9.2 million USD (publicly stated) | Early 2027 (long-dated) |

Nvidia |

Puts | About 187 million USD | 1 million shares | Not disclosed, but likely low single-digit percent of notional | Likely multi-quarter |

Together, these two positions account for roughly 80 percent of Scion’s reported equity exposure by notional value. On Palantir, Burry has even clarified that he spent about 9.2 million dollars in premium for this 912 million dollar notional position, with options that only expire in early 2027. In other words, he is risking single-digit millions to control three-digit millions of downside exposure on the poster children of the AI boom.

What is Burry seeing in AI?

Across his tweets and shared charts, the core of Burry’s current thesis is quite simple:

1. Cloud growth is slowing, AI capex is exploding.

Internal charts he posted compare 2018-2022 cloud revenue growth at Microsoft, Amazon and Google to 2023-2025. Growth has decelerated from 20-40 percent to mid single digits, even as capital expenditure on AI infrastructure is ramping to levels last seen around the dot-com peak. Revenue momentum is fading while spending goes vertical. That is not operating leverage. That is a strain.

2. A circular AI economy, not a clean demand cycle.

Burry highlights the “closed loop” of money flows: hyperscalers and incumbents invest in AI start-ups, those start-ups buy Nvidia chips, those chips run on the same hyperscalers’ clouds, which then report “AI demand”. Capital is chasing itself in circles. Genuine, high-margin end demand is far less visible.

3. Palantir - great story, brutal math.

At the heart of the trade is Palantir. The company’s valuation has stretched into territory where investors are effectively paying triple-digit multiples of revenue and hundreds of times earnings to own the stock. The transcript you shared talks about investors paying around 100 times revenue and roughly 700 times earnings at one point. Growth, while strong, is already decelerating and heavily sales-and-marketing driven. Burry’s view is straightforward: the expectations embedded in the price are impossible to meet without a perfect runway of compounding, zero competitive pressure and zero regulatory friction.

4. Nvidia - picks and shovels at peak cycle.

Nvidia has been the main “picks and shovels” winner of the AI rush, briefly touching a multi-trillion-dollar market cap with stock performance that has dominated global indices. The entire bull case rests on AI infrastructure spending compounding for years. Burry’s concern is that this capex curve is already running ahead of monetisation. If customers eventually discover that the incremental dollar of AI spend is not generating a commensurate return, the first thing they cut is new hardware orders. At current valuations, even a plateau in growth, not a collapse, can compress the multiple sharply.

5. Macro backdrop: a market priced for perfection.

Burry’s AI scepticism sits inside a broader view that US equities are structurally expensive. He has pointed to indicators like the Buffett Indicator (Wilshire market cap to GDP) well above historical peaks and a Shiller PE that is back in the 40s, levels seen only around the 1929 and 1999 extremes. In that world, AI leaders are not just good businesses. They are also the most crowded and valuation-stretched part of an already stretched market.

However, the financials tell a different story. Though the valuations have skyrocketed as Palantir moved from a loss making venture to a profit earning one, it still is growing, at a super fast rate. The key question remains, will it be Bury’s thesis or the AI boom to stand victorious over the next few quarters.

Conclusion: The Winner Will Be Decided by Gravity

The standoff between Michael Burry's thesis and the AI boom is not a debate over technology; it's a conflict between financial math and market momentum.

Palantir and Nvidia are indeed driving a powerful technological revolution, but they are doing so within a structurally strained ecosystem. Burry’s analysis, that slowing cloud revenue is being outpaced by exploding AI capex, reveals a significant financial paradox. Furthermore, the "circular economy" where capital chases itself in closed loops, rather than clear external demand, suggests the growth narrative is artificially inflated.

Burry is betting on the inevitable return of financial gravity. His thesis is simple: when the music stops, when interest rates truly bite, or when customers realize the massive AI spend doesn't yield an immediate ROI, the most extended valuations suffer the most.

With Palantir trading at a P/E over 400 and the broader market indicators flashing Dot-Com-era extremes, the system has no margin for error. The AI leaders must execute flawlessly for years just to justify today's prices. Any failure, technological, regulatory, or competitive, will lead to a savage multiple compression.

Maybe, Burry's thesis will prevail in the short-to-medium term, perhaps. Gravity always wins. While AI will transform the world, the valuation gap between price and reality is too wide.

Or will it not? The question persists whether to trust Burry’s pedigree or the AI boom.

If you'd like to discuss your portfolio or explore how Xylem can help you navigate this market, consult with us here.

Comments